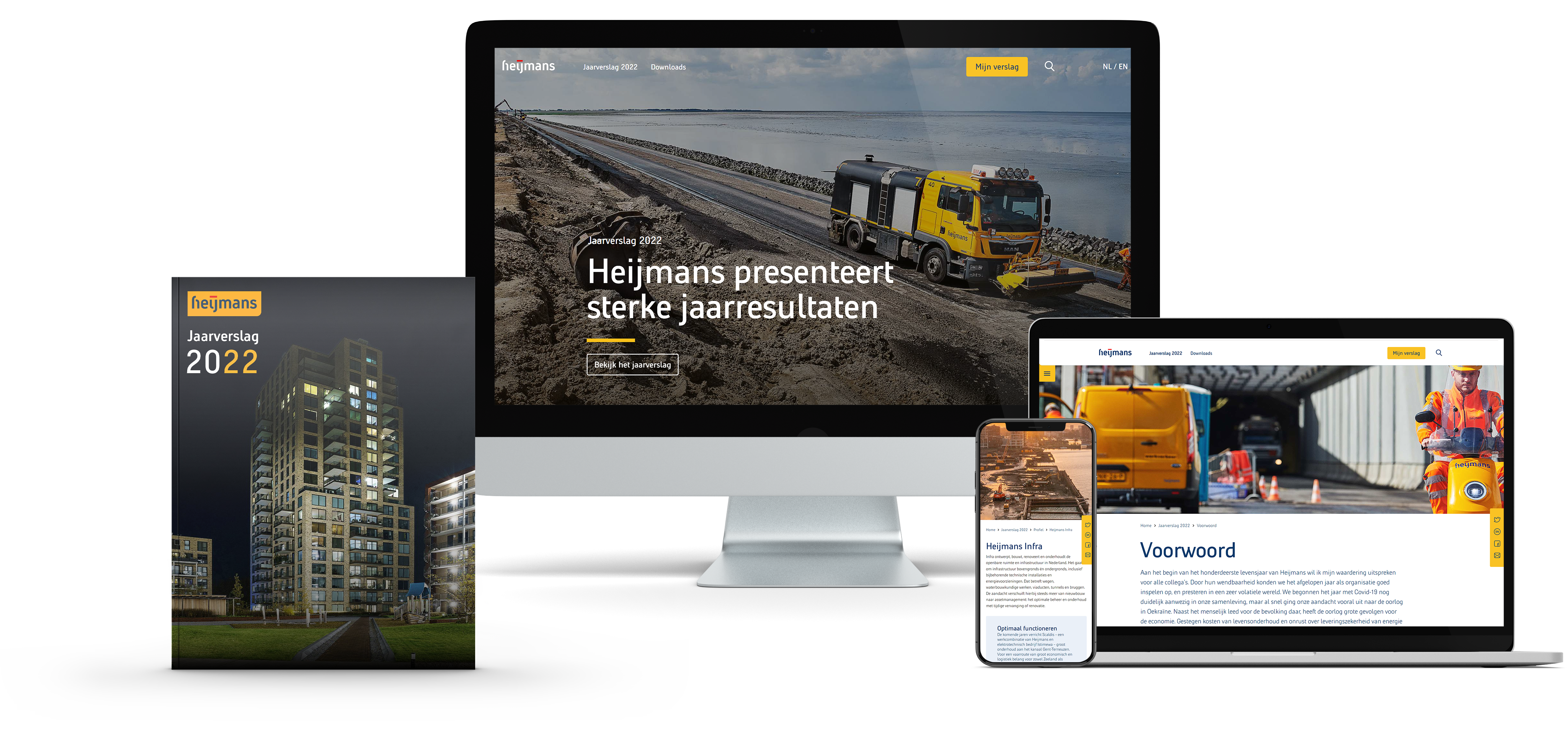

At F19 Digital Reporting, we are dedicated to developing the most user-friendly software for streamlining the ‘last inch’ of reporting: the complex final stage of the reporting process where a fully designed report must be published in various formats, including inline XBRL, which is the mandatory format for ESEF and CSRD reports.

The F19 platform does just that:

It enables end users to import and combine content and data from various systems and sources.

End users can easily adjust the content and layout themselves, tag it, and safely co-create the report with their creative agency.

When ready, end users can publish the report in various formats from one single source: For example, as a website, as a PDF and as native iXBRL. Besides, because the F19 platform is a headless content management system (CMS) our experienced partners can develop tailor-made applications that are future-proof. End users can collaborate with them to create an engaging media mix that exceeds stakeholders’ expectations.

Do you wish to learn more? Then please contact us for a free demo. We are happy to show you all the benefits of Digital-First, multichannel reporting with F19.